The management presentation was impressive.

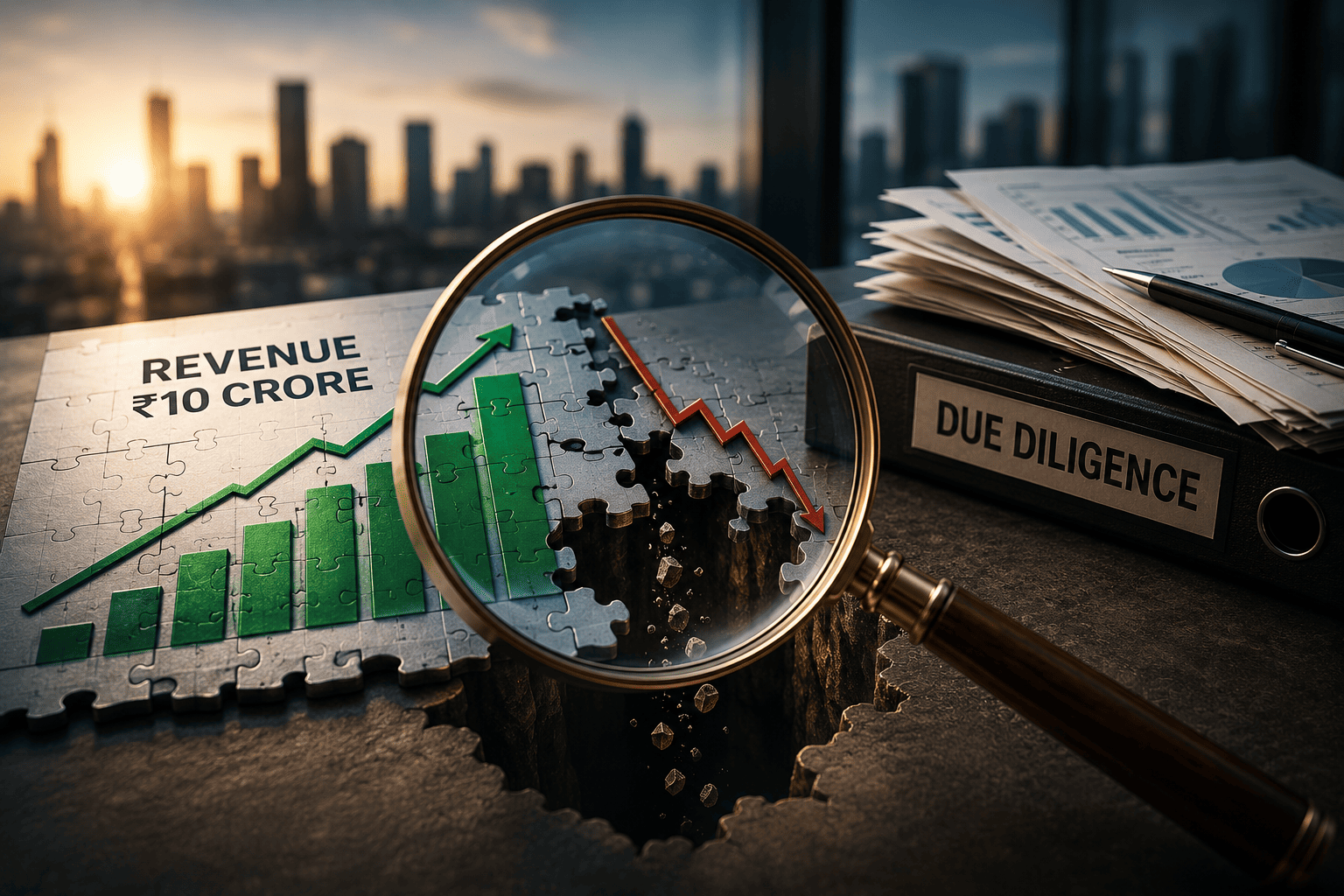

Revenue had crossed ₹10 crore.

Year-on-year growth exceeded 80%.

Customer acquisition was accelerating.

The founders knew every growth metric by heart. They could explain their market opportunity, customer pipeline, and expansion plans in remarkable detail.

Investor interest was strong.

Then financial due diligence began.

One question surfaced within the first few days of the review:

"Can you help us understand why operating cash flow is negative despite strong revenue growth?"

The answer wasn't immediately clear.

And that became the real issue.

The Red Flag Wasn't Revenue. It Was Cash Conversion

At first glance, the business appeared healthy.

Revenue had increased consistently over the previous three years. Gross margins were improving. Customer numbers were growing.

Yet the cash position told a different story.

During the review, investors noticed that receivables had increased significantly faster than revenue.

While revenue had grown by approximately 80%, trade receivables had more than doubled during the same period.

Nearly 40% of outstanding receivables were over 180 days old.

This immediately shifted the discussion.

The question was no longer:

"How fast is the business growing?"

It became:

"How much of this reported revenue is actually converting into cash?"

That distinction matters.

A startup does not fail because revenue is recorded.

It fails when cash does not arrive.

Revenue Quality Matters More Than Revenue Growth

One of the most common misconceptions among founders is that investors focus primarily on revenue growth.

In reality, sophisticated investors spend considerable time assessing revenue quality.

During financial due diligence, investors often ask questions such as:

- How much of reported revenue has been collected?

- Are customers paying within agreed credit periods?

- Is growth being supported by aggressive payment terms?

- Are collections keeping pace with sales?

- How much working capital is required to sustain growth?

These questions help investors understand whether growth is self-sustaining or dependent on continuous external funding.

In this case, the concern was not that revenue had been overstated.

The concern was whether future growth would require significantly more working capital than management anticipated.

For investors, that translates directly into risk.

The Three Questions Every Investor Asked

As diligence progressed, three recurring questions emerged.

1. Why Are Receivables Growing Faster Than Revenue?

Receivables naturally increase as businesses grow.

However, when receivables expand significantly faster than revenue, investors want to understand why.

Were customers demanding longer payment terms?

Had collection efforts weakened?

Were invoices being disputed?

Or was the company pursuing growth at the expense of cash discipline?

Each possibility carried different implications.

2. How Much Revenue Has Actually Turned Into Cash?

This question often reveals more about a business than the revenue figure itself.

A company reporting ₹10 crore in revenue sounds attractive.

A company that has collected only a fraction of that revenue presents a different investment proposition.

Investors wanted to understand the cash conversion cycle, debtor ageing trends, and collection efficiency.

They were not questioning growth.

They were evaluating sustainability.

3. Will Future Growth Require More Capital?

This ultimately became the most important question.

If revenue doubled again next year, would receivables double as well?

Would additional funding be required simply to support working capital?

Would the business generate cash or continue consuming it?

The answers directly influenced investor expectations and risk assessments.

What the Cash Flow Statement Revealed

Many founders spend significant time reviewing their profit and loss statement.

Far fewer spend the same amount of time analysing cash flow.

That is often where the most important insights exist.

The cash flow statement revealed that increasing receivables were absorbing a substantial amount of cash.

Growth looked impressive on paper.

The bank balance suggested a different reality.

This did not mean the business was weak.

It meant the business had a working capital challenge.

The distinction is important.

Financial due diligence is rarely about finding reasons to reject a company.

It is about understanding the underlying drivers of performance and identifying risks that may not be immediately visible.

The Impact on the Investment Discussion

The company ultimately remained attractive.

Customers were genuine.

Revenue growth was real.

Market demand was strong.

However, the diligence findings changed the nature of the conversation.

Discussions shifted from growth alone to growth quality.

Investors wanted greater visibility into collections.

Additional reporting requirements were introduced.

Working capital assumptions were revisited.

Future cash requirements became a key area of analysis.

The issue did not kill the deal.

But it influenced how the deal was evaluated.

And that is exactly why financial due diligence exists.

The Lesson for Founders

Every founder knows their revenue number.

The best founders understand the journey from revenue to cash.

Before entering a fundraising process, ask yourself:

- Can you explain changes in operating cash flow?

- Can you explain your debtor ageing profile?

- Can you explain why receivables increased?

- Can you explain your cash conversion cycle?

- Can you explain how future growth will impact working capital?

Because when investors begin their review, they are not merely validating revenue.

They are assessing whether that revenue translates into sustainable, investable growth.

Revenue attracts attention.

Cash conversion builds confidence.

And confidence is what ultimately drives investment decisions.

Need help applying this insight?

Our consulting team helps businesses translate strategy into practical action.

Talk to our team →